Disabled People Are the Canaries in the Coal Mine

The disabled community has responded to the adversities they face by organizing for legal rights that protect their autonomy and access to public life. But these rights are increasingly under attack.

It may be wise to avoid this source for your asset management, because two months later in the same newspaper you discovered that the spread of euro prosperity did not survive into July, “a slowdown in the eurozone’s recovery was confirmed on Thursday [3 July], after the final reading of a poll of purchasing managers hit is lowest level this year”.

The fleeting apparition of recovery brings to mind the occasional reports of earthly visitations of Christian saints, which bring ecstasy to the observer but prove transitory in their broader impact. Transitory the alleged recovery has been to say the least, as confirmed by both the New York Times (return to recession in France) and the International Business Times (manufacturing slowdown in Germany).

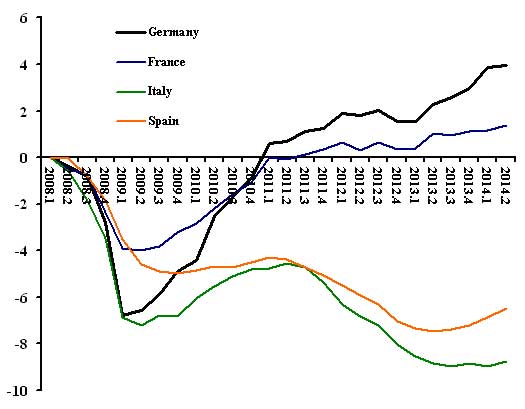

As I demonstrated a month ago, the so-called recovery was not “real”, nor brief and fleeting. It has yet to occur. The chart below, up-dated with preliminary statistics for the second quarter of 2014, demonstrates the euro recovery that never was. Of the four largest economies on the euro zone, the “best performer”, that of Germany, is a merger four percent above its level at the beginning of 2008.

And that only starts the bad news. The economies of two countries, Italy and Spain, are at a lower level of GDP than at the depth of the Global Crisis of 2008-2009. For these two countries returning to the lowest point of the worst recession in eighty years would be an improvement. That might be taken as a working definition of “been down so long it looks like up to me“.

GDP compared to 2008: Largest 4 EU economies (percentage points, 2008 1st quarter = 0)

Source: www.oecd.org/statistics.

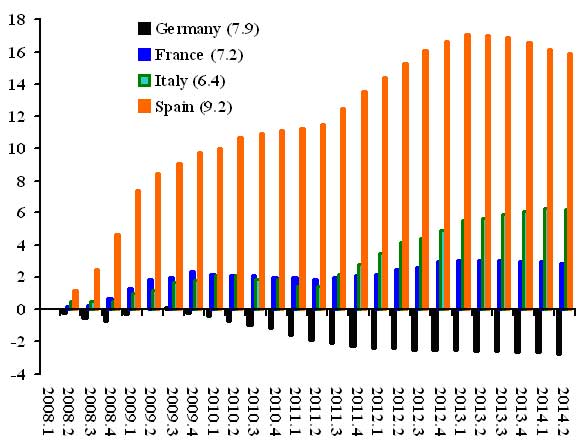

The news for national income is bad and for unemployment even worse. The chart below shows the percentage point change in unemployment rates, again compared to the first quarter of 2008. Setting the first quarter of 2008 as zero allows easy visual comparison. For only one country, Germany, is unemployment lower, 5.1% of the labor force now compared to 7.9 at the beginning of 2008.

Among the others, the unemployment rate is 16 percentage points higher in Spain (at 25% of the labor force), six higher in Italy and three in France. Only for Spain do we see improvement, if that word applies to a change from 26.3 to 25.1%.

Unemployment rates compared to 2008: Largest 4 EU economies

(percentage points, 2008 1st quarter = 0, numbers in legend rates for 2008Q1)

Source: www.oecd.org/statistics.

What is going on in the euro zone? Market economies are supposed to grow, driven by the “animal spirits” of capitalists (to use the term coined by John Maynard Keynes). What is the cause of the stagnation that seems to affect even the Teutonic dynamo? The answer is quite straight-forward and obvious to all those not blinded by ideology -- a lack of demand.

Businesses produce things when their owners think those things can be sold. They can be sold domestically to other businesses (capital goods), to households (consumer goods), to the public sector (government demand), or to foreign markets (exports). The austerity policies championed by the German government and enforced on euro zone countries by the European Commission have public expenditure contracting in real terms in most countries.

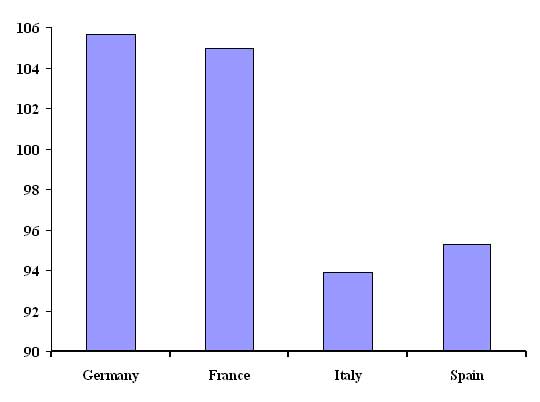

The chart below tells the public expenditure story. In constant prices, public expenditure in Germany was six percent higher in 2013 than in 2008, and five percent higher in France. Both countries grew compared to 2008, albeit by not very much. In Italy public expenditure was down by 6% and by 5% in Spain. The economies of both countries contracted compared to 2008. There is a lesson from those numbers -- don’t cut spending in a recession.

Ratio of public expenditure in 2013 compared to 2008, 4 largest euro economies

(constant prices)

Source: www.oecd.org/statistics.

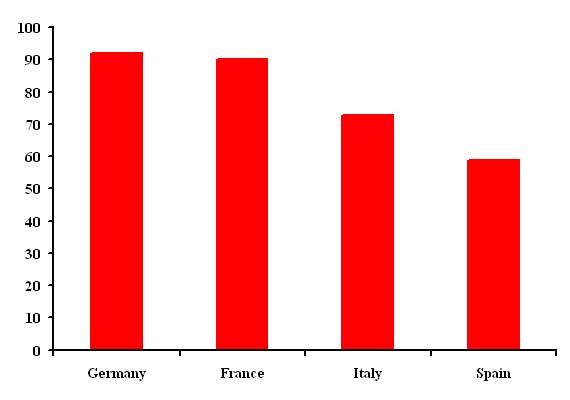

What of the animal spirits of the private sector? Bad news again, with private investment lower in all four countries in 2013 compared to 2008. The falls are 8% for Germany, 10% for France, a debilitating 27% for Italy, and a disastrous 41% in Spain. As for exports, virtually no change for France and Italy in constant prices (up 2% and down 2%, respectively). Germany exports increased by 10%, sufficient to compensate for the fall in investment and stimulate a bit of growth. But in Spain not even a 20% export increase could raise the economy off rock-bottom in face of the declines in private investment and public expenditure.

Ratio of Private Investment in 2013 compared to 2008, 4 largest euro economies

(constant prices)

Source: www.oecd.org/statistics and www.worldbank.org..

Has recovery come to the largest countries of the eurozone? No, because austerity has depressed public-sector demand. The low growth or decline in public expenditure has lowered private-sector growth expectations, keeping investment low. And except in Germany increases in exports have been less than the contraction in private investment.

Public expenditure down, private investment dismal, and export growth inadequate to keep the total demand for goods and services from falling. What about households (aka “consumers”)? No prizes for figuring out what happens to household expenditure when unemployment continues at a high rate and other sources of demand stagnate.

But, isn’t all this austerity, public and private, the necessary price to pay for running up those huge public debts and budget deficits? That’s a story for another day. I show in chapter 9 of my new book, Economics of the 1%, austerity and slow growth make both debt and deficits worse. Which leads to the one-liner of the euro economies -- they suffer from policy-induced stagnation, self-inflicted. Stop the policy sabotage of these economies and growth will return It really is that simple.

--John Weeks