U.S. Banks and the Dirty Money Empire

Reprising a classic article by radical sociologist James Petras, who died on January 17th, 2026.

(1) New Economy Week: It's New Economy Week! Sponsored by the New Economics Institute. I have just two related items to mention:

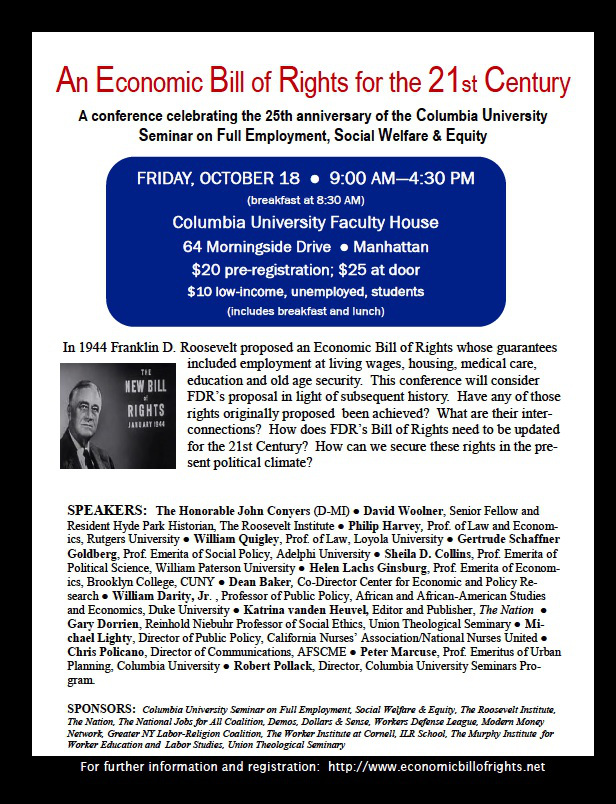

(2) An Economic Bill of Rights for the 21st Century--A Conference: This Friday (the 18th) there will be a conference celebrating the 25th anniversary of the Columbia U. Seminar on Full Employment, Social Welfare, & Equity, co-sponsored by a bunch of great organizations, including D&S. See the flyer at the top of this post for more info. Get the pre-registration discount ($20 instead of $25) if you register in advance. More details here.

(3) The So-Called "Nobel" Prize: When Ratzinger became pope, I decided that I was going to stop going along with the whole re-naming charade--I never shifted from Ratzinger to Benedict. (Ok, it was easy with him--I am finding it harder to keep with Bergoglio vs. Francis, partly because Bergoglio is hard to remember, and partly because Francis is turning out to be surprisingly cool, at least in comparison with the popes since John XXIII.) I am thinking we should similarly refuse to call the economics Nobel "Nobel," given that it isn't really a Nobel--given instead by the Swedish central bank, and only since 1968. So let's call it the Sveriges Riksbank "Nobel" Prize. Here are some items related to the 2013 award to Eugene Fama, Lars Peter Hansen, and Robert Shiller:

I'll have more stuff to post on the SR"N" Prize soon.

(4) More on Shutdown and Debt Limit: Two notable items:

I just heard about this on Thom Hartmann's program (thanks Thom!).This is apparently Rep.Ron Paul's idea that has been taken up and supported by Rep. Alan Grayson (so how bad can it be!).As the Fed routinely does not collect interest on Treasury Bills that it "buys" from the Gov. with money that it creates out of thin air, there is really no reason to keep this "debt" on the books at all. Cancelling the $ 2.1 Trillion of U.S. Gov. Debt held by the Fed could keep us below the self imposed and utterly artificial "debt limit" crisis, at least for a while. Apparently the Fed has the authority to do this. The Fed does not need to cancel all of its $2.1 Trillion. It could retain a sufficient stock of T-Bills to engage in normal open market operations.See: http://www.marketoracle.co.uk/Article42663.html for some reporting on this.[There's also a piece about this on one of the Financial Times blogs: Will Central Banks Cancel Government Debt? But you have to register for the FT to read it. It's not hard to do so, though.}

This strategy shreds any remnants of trust in the competence and ability of government, and sells the ludicrous notion that the private sector is the solution to societal problems.

These forces have prevailed in some parts of Europe, forcing governments to shed social services to the poor, the unemployed and the young. Those governments have created crises, but they have hardly solved them. Indeed, they have exacerbated them.

Such societies aren’t merely unequal; they have stoked social and class conflict.

Several decades ago, American economists (from the Chicago School of Economics) preached austerity throughout Latin America. Their economic recipes brought chaos, disaster and mass pain.

Naomi Klein has written movingly about such experiments, which ripped nations apart, in her 2007 work, The Shock Doctrine.

Now, it is here – disguised – but here. Schools are closing; repressive institutions are multiplying, and jobs are paying less and less.

Meanwhile, the 1% (remember Occupy?), the richest percentile of Americans, have made more money recently than at any previous period in the nation’s history.

This isn’t just a conservative program; it is also a neo-liberal program that prays at the holy altar of Wall Street.

The neo-liberal program of surrender to market forces has strengthened and energized rightist tendencies, and made the market the very center of national life: not the People.

So, schools close one day; governments shut their doors the next.

The Market prevails.

---© ’13 maj

That's it for today.

--Chris Sturr